The IndeX Files 22-11-2022

Equities Rally Pauses Amidst Fed Hawkishness

It’s been a rather muted start to the week for benchmark global equities indices. On the back of the wave of better risk appetite we saw following the US October CPI report, markets have lost their shine due to a combination of better-than-expected US retail sales, hawkish Fed commentary and fresh fears regarding China lockdown risks.

Market pricing for a large Fed hike in December is creeping up again in response to recent Fed comments. Last week, we heard Fed’s Daly calling for the Fed to hike rates beyond the current projected peak. This week, Fed’s Mester echoed that sentiment saying that Fed policy needed to be more restrictive, and that the Fed was “barely there” on rates so far. If this recent theme continues, and particularly if we see any upside surprise in the next inflation report, equities might well turn lower again.

China Lockdown Fears

On the China front, news this week of two fresh covid deaths in Beijing have sparked concern that the region might be headed for fresh lockdowns. With China still sticking to its zero covid policy for now, there is a real risk of such measures being announced, particularly if further fatalities are noted. With plenty of market focus recently on potential reopening in China, such news would likely fuel sharp downside in equities markets, reflecting disappointment.

Technical Views

DAX

The breakout above the bearish trend line from YTD highs is holding for now. Price is currently sitting atop the 14170.79 level and with both MACD and RSI bullish the focus is on a continuation higher towards the 14703.98 level next. To the downside, 13672.31 is the nig support to note.

.png)

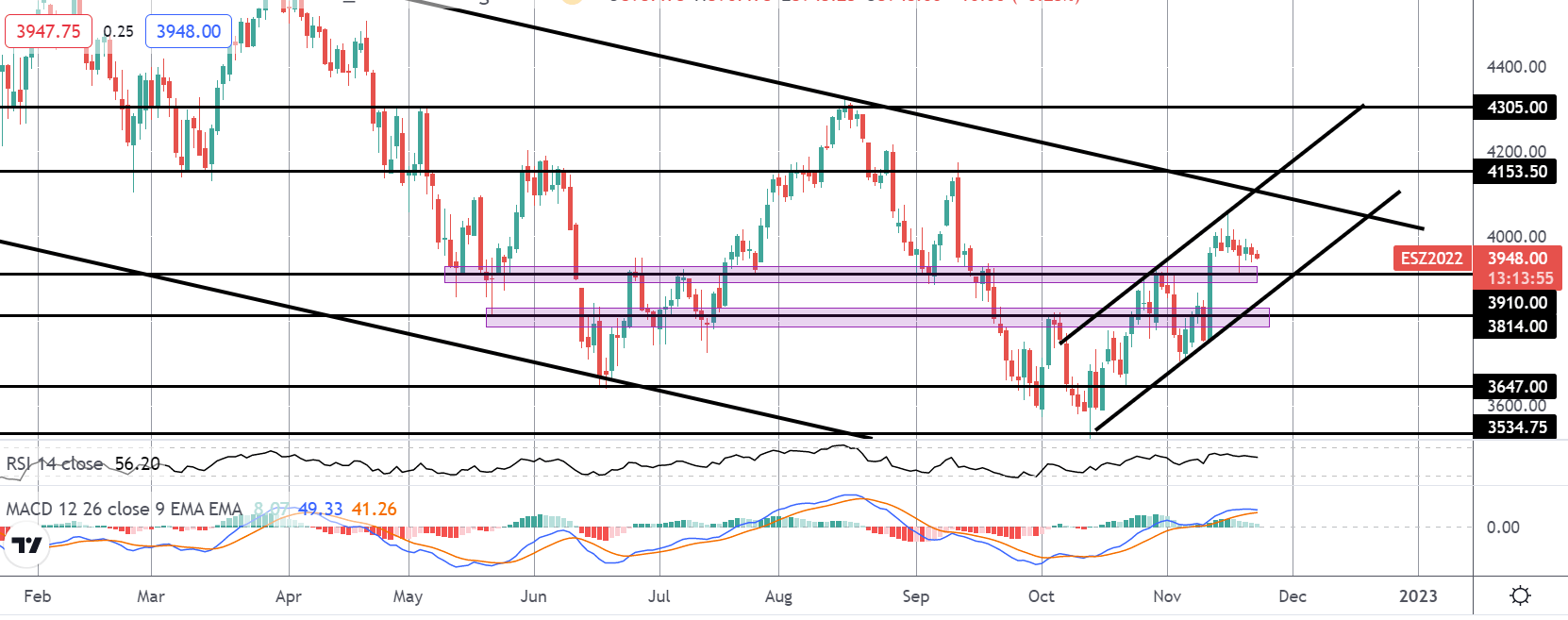

S&P 500

The rally in the S&P, framed by the corrective bull channel off the YTD lows, is fast approaching a test of the bearish trend line from YTD highs. This is a key area for the market and a break above there will be firmly bullish. To the downside, initial support is at the 3910 level, underpinning price currently, with 3814 and the bull channel low sitting beneath.

FTSE

The rally off the YTD lows is continuing with the index attempting to break higher again this week. Price is fast approaching a test of the bear channel top, with structural resistance at 7575.8 – 7678.8 sitting just above. With momentum studies supportive, outlook remains bullish while the market holds above 7362.6.

.png)

NIKKEI

The rally in the NIKKEI stalled into a test of the 28356.6 resistance last week. However, the recent bull move remains intact, with momentum studies supportive, and while price holds above the 27422.9 level, the focus is on a breakout higher and a continuation towards the next resistance level at 29464.9

.png)

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.